The Private Credit Crisis: Why 2026 Is Different

The $1.5 Trillion Illiquidity Bomb

DONT HAVE TIME? WE GOT YOU COVERED...

THE REAL UNDERLYING ISSUE…

The Private Credit Crisis: Why 2026 Is Different

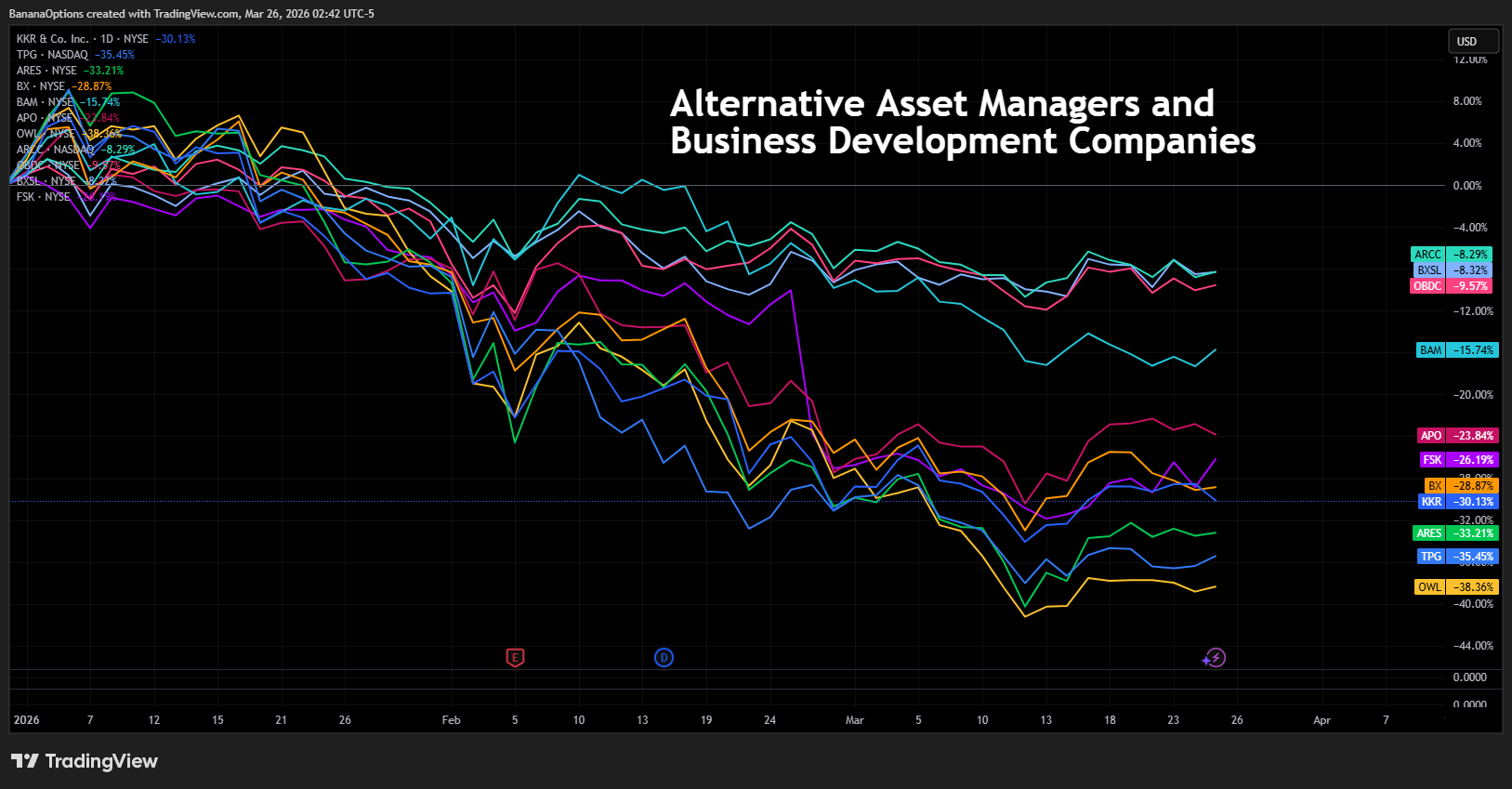

Private Credit funds have increasingly taken money from pension funds, insurers, and even retail investors, promising high yields and steady returns. Investors are generally told they can request their money back on a set schedule. However, the PC funds do not hold cash. Their money is locked up in 5 to 7 year illiquid loans made to mid sized companies. We are actually watching this mechanical failure play out right now in early 2026. As anxiety over the economy and AI bubbles rises, investors are trying to pull their capital out. Because the funds cannot quickly sell these bespoke, illiquid loans to raise cash, they are forced to impose redemption gates literally locking the doors and refusing to give investors their money back, with some major funds recently capping withdrawals at just 5%. When investors realize they are trapped in a burning building, the panic mechanically accelerates. Another massive issue is the Private Equity maturity wall. During the zero interest rate frenzy leading up to 2022, PE firms bought thousands of companies using massive amounts of floating rate debt. Debt has an expiration date, and we have now hit a massive maturity wall in 2026 and 2027 where trillions of dollars of this corporate debt must be refinanced. These buyouts were underwritten with the assumption that interest rates would stay near zero. Now they must refinance in a world where debt costs 8% to 12%. If a PE owned company's cash flow cannot cover the new, massive interest payments, it mechanically defaults. There is no sentiment involved. it is just a math equation they can no longer solve. To avoid officially defaulting on these expensive loans, many PE backed companies are relying heavily on a toxic feature called Payment In Kind, or PIK. PIK allows a struggling company to defer paying cash interest. Instead, the interest owed is simply added to the total principal balance of the loan. PIK is the corporate equivalent of paying your mortgage with a credit card. It keeps the official headline default rate looking artificially low, hovering under 2%, giving a false sense of security. But the true distress rate is dramatically higher. Eventually, the debt burden compounds to a size that mathematically crushes the company, wiping out the equity and severely burning the private credit lenders. This ties directly back to the AI narrative we discussed earlier through software cross contamination. A massive portion of the Private Credit boom was fueled by lending to legacy Software as a Service companies, banking on their recurring revenue models. PC lenders assumed these software revenue streams were sticky, predictable, and recession proof. However, AI is aggressively disrupting these legacy, seat based software models. Companies are realizing they can replace expensive SaaS subscriptions with internal AI agents for a fraction of the cost. As the valuations and revenues of these underlying software companies plunge, the private credit loans backing them turn into toxic waste. The 2008 parallel is incredibly clear here. In 2008, the system broke when the market realized the AAA mortgage bonds were garbage, but there was no liquidity to sell them. In 2026, the trigger is investors realizing their safe, high yield private credit funds are backed by over leveraged companies slamming into a maturity wall, and the exit doors are padlocked.

Other news

Commercial Real Estate’s "Extend and Pretend" Era Ends • While Private Credit dominates the headlines, the Commercial Real Estate (CRE) sector is hitting its own maturity wall. Billions in commercial mortgage-backed securities (CMBS) are coming due this quarter. With office vacancy rates still hovering at record highs and borrowing costs double what they were in 2019, regional banks are finally being forced to mark down their CRE portfolios to reality. Fire sales of Class-B office buildings in major metros are accelerating, often clearing at 40% to 60% discounts from their peak valuations. The SEC Circles the Private Credit Wagons • In response to the rising number of retail and pension funds trapped behind redemption gates, regulatory bodies are waking up. The SEC is reportedly drafting emergency transparency rules that would force Private Credit funds to publicly disclose their true ratio of Payment-In-Kind (PIK) loans to cash-performing loans. Insiders suggest the lobbying pushback from Wall Street is massive, as forced transparency could instantly trigger the exact panic the funds are trying to suppress. AI "Agents" Begin Hollowing Out Middle Management • The AI disruption isn't stopping at legacy SaaS platforms. Major enterprise firms have reported a sudden 15% drop in middle-management and junior white-collar hiring for Q1 2026. The culprit? The widespread deployment of autonomous AI agents that can now handle end-to-end workflows in procurement, basic legal review, and entry-level accounting. Corporate cost-cutting is shifting from mass layoffs to a permanent "hiring freeze" for roles that can now be outsourced to a $500/month compute cluster. Capital Flight to "Liquid" Safe Havens • As anxiety over locked-up capital in private funds grows, there is a visible rotation back into highly liquid, traditional safe havens. Gold is seeing sustained record inflows, and short-term US Treasuries remain the default parking spot for institutional cash. Investors are learning the hard way that an 11% promised yield means nothing if the exit doors are padlocked.